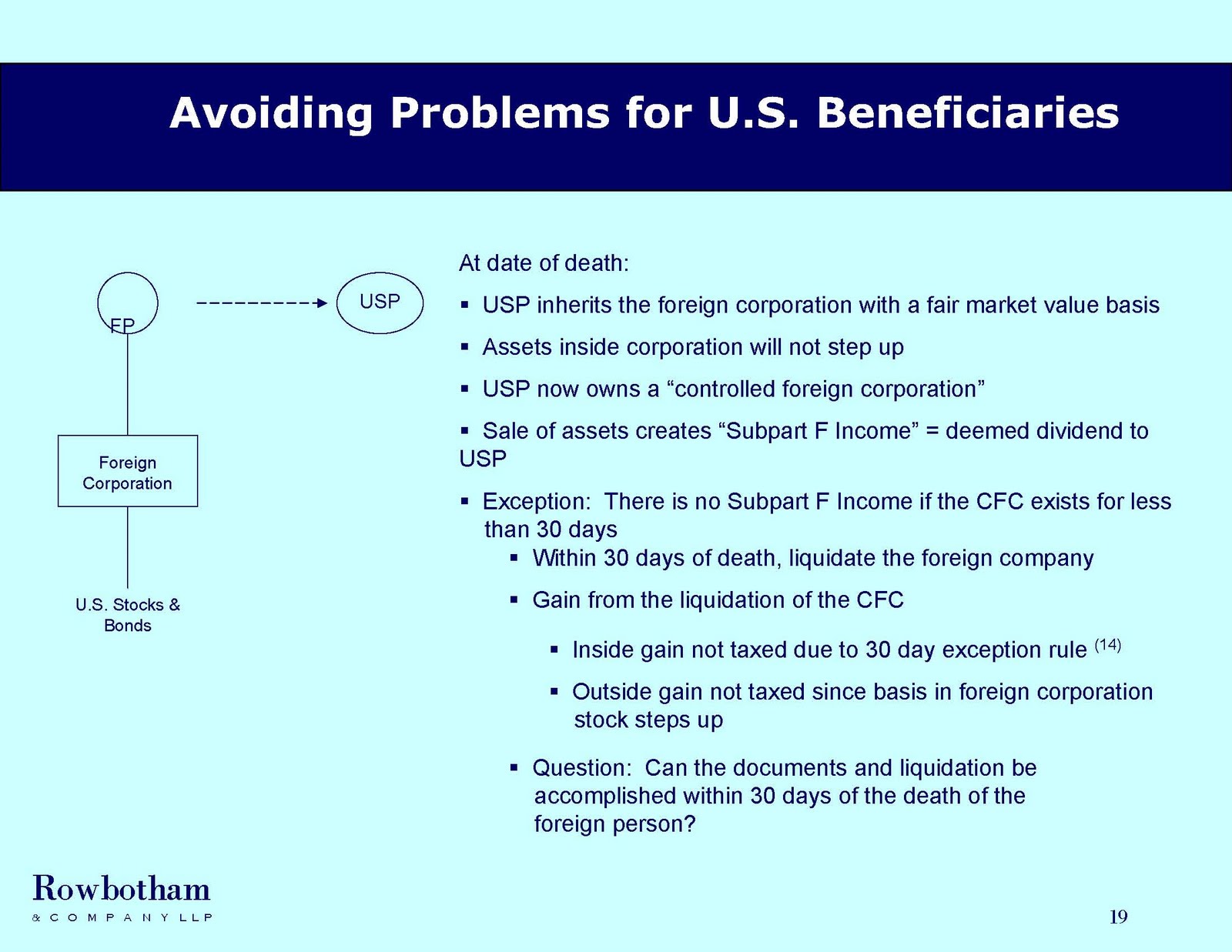

Heavily entrenched in our tax system is the view that wealth accumulation by any citizen or resident is U.S. U.S. , but in Asia .

Faced with U.S. tax burden and erroneous reporting rules on foreign income and wealth that some consider unjustified, many wealthy U.S. citizens and residents of Asian origin are considering doing what a decade ago would have been unthinkable – giving up their green cards or citizenships as a wealth preservation strategy. Unless the current U.S.

In December 2010, IRS Commissioner, Doug Shulman, stated that cleaning up abuses and mounting a greater attack on tax evasion is the order of the day. International tax evasion is the number one offense on the IRS’s top ten areas of tax evasion schemes. Another more recent example is the Department of Justice action. They issued a summons on the Hong Kong and Shanghai Banking Corporation of India (HSBC India) that requires the bank to turn over information on U.S. Singapore , India and Hong Kong . China

Background

In the 1970s, 80s and 90s India India entered the best American universities, graduated in large numbers with engineering degrees, found jobs, obtained green cards and ultimately obtained their U.S. Silicon Valley ’s boom. U.S. citizenship was itself a treasured goal: it was the escape hatch from restrictions imposed by India U.S. citizenship also provided an evergreen ticket to sponsor family in India to immigrate to the U.S. India ’s businesses started to flourish in part due to the Silicon Valley training with many returning to India with a green card or a U.S.

In 1999, India India , turning sleepy cities like Bangalore

Today, families inIndia India U.S. citizens and green card holders, and this new wealth is now trapped inside the U.S. U.S.

Today, families in

1. All or most of the wealth is in India , not the U.S.

2. Families and advisors living in India are unfamiliar with U.S.

3. To get things back on track, as many wish to do, the penalties due to nonreporting in past years is enough to humble Warren Buffett.

The U.S. U.S. India , are now being advised about the U.S.

Procedures exist that allow U.S. citizens to expatriate which has the effect of terminating their ongoing U.S. U.S. taxes for the past five years exceeded $125,000, then the U.S. U.S. citizenship in the first place, as well as ties to family now entrenched in the U.S. U.S.

On a recent trip to India

Savvy financial institutions and international tax advisors are busy mapping out strategies. For many wealthy Indians, negotiating these rules is like driving in the streets of Mumbai – you can’t survive merely by following the rules in the motor vehicle code. In order to properly expatriate and properly exit the U.S. tax system, a person needs to submit five years of properly filed U.S. India may one day impose gift and estate taxes, holding U.S. citizenship may still be a good hedge if the tax system in India India

In February, the IRS announced an amnesty program whereby individuals can voluntarily file past returns with the correct tax and discloses. By doing so, potential criminal charges are waived and the 50% penalty on undisclosed foreign accounts will be reduced to 25% for accounts in excess of $75,000. For example, if one has an undisclosed foreign account of $1 million, even if the additional income and additional tax is minor, the penalty for not filing the annual Treasury Form TDF 90-22.1 is $250,000. The scope and amount of the penalties are confiscatory and appear unfair to many, since the wealth was generated outside the U.S. and in many instances has already been taxed in India

Like it or not, U.S. U.K. immigration law being implemented specifically to attract the global high net worth person to take on UK U.K.

The SolutionCongress might not like to the bitter pill of liberalizing the expatriation rules for a group of high net worth individuals that appear on the surface to be tax evaders. It will take some reflection and forward thinking to solve the problem in a way that is beneficial to both foreign residents and to the U.S. Treasury. The U.S. Tax Code can stick with assumptions that are no longer valid, or Congress needs to reconsider how to keep all of its citizens and residents within the system. Otherwise, vast amounts of wealth will stay outside the U.S. - undeclared and untouchable by U.S. U.S.

Congress needs to heed the prophetic words from one of Bob Dylan’s songs in the ‘60s:

Come Senators, Congressmen, please heed the call

Don’t stand in the doorway, don’t block up the hall

For he that gets hurt will be he who has stalled

There’s a battle outside and it is ragin’

It’ll soon shake your windows and rattle your walls

Oh, the times they are a-changin’.